minute read

In February 2023, the U.S. EPA finalized and released its Clean Water Act Financial Capability Assessment (FCA) Guidance, which is used to consider the economic impacts of Water Quality Standard decisions and negotiate implementation timelines for sewer permits and enforcement agreements. Now that the FCA Guidance has been out for more than a year, we’re sharing our experience using the new guidance from a practitioner’s perspective.

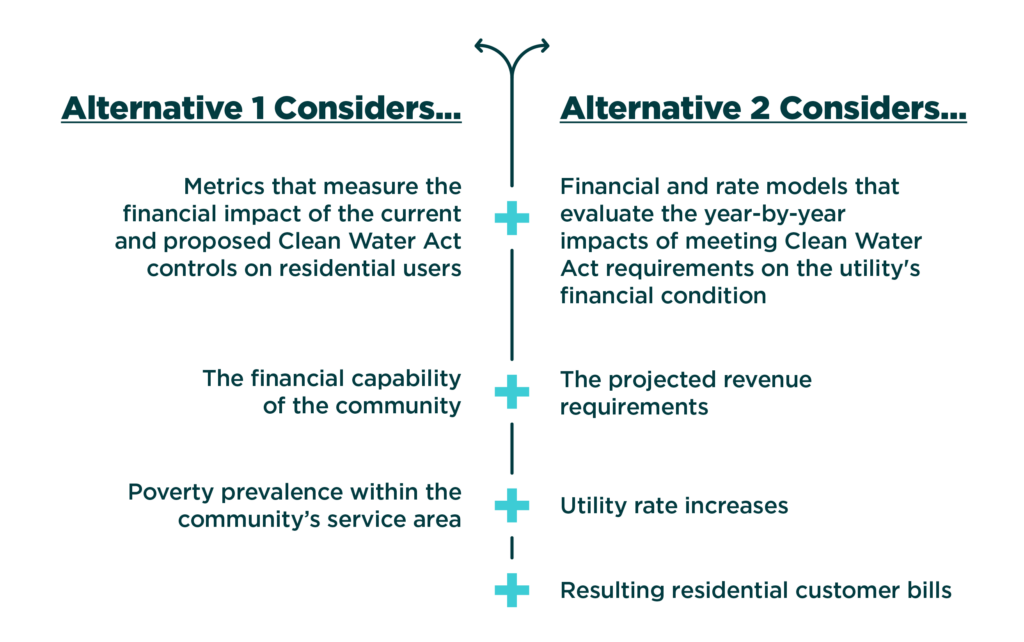

The FCA Guidance sets forth two alternatives that communities can employ to assess their financial capability when negotiating compliance schedules. Alternative One considers metrics that measure the financial impact of the current and proposed Clean Water Act controls on residential users, the financial capability of the community, and the poverty prevalence within the community’s service area. Alternative Two uses financial and rate models that evaluate the year-by-year impacts of meeting Clean Water Act requirements on the utility's financial condition, the projected revenue requirements, utility rate increases, and resulting residential customer bills.

The new 2023 FCA Guidance includes expanded metrics under Alternative One that consider poverty prevalence by comparing several indicators to national figures. These include the upper limit of the lowest quintile income, the percentage of the population with income below 200% of the Federal Poverty Level, the percentage of households receiving SNAP benefits, the percentage of vacant housing units, and the percentage of unemployed adult population in the civilian labor force. While these additional metrics help to provide a more complete picture of a community’s financial capability, the metrics used in Alternative One and their comparisons to national averages still suffer from many of the same shortcomings as the previous 1997 EPA Guidance that have been widely recognized and documented. These include:

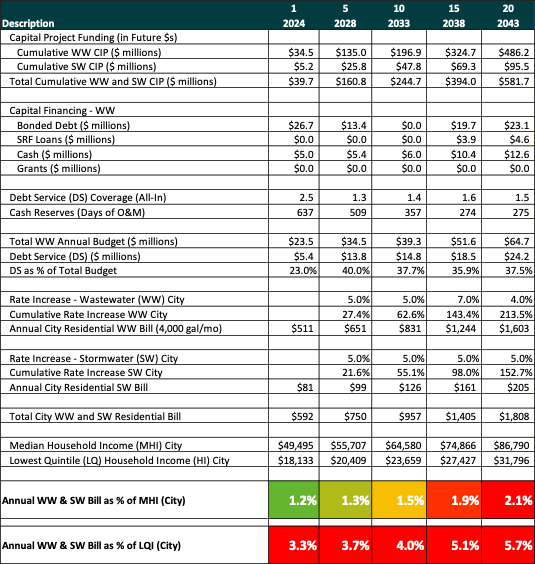

Given these shortcomings, our experience has been that utilities completing FCAs largely ignore Alternative One and select the Alternative Two option or complete both Alternatives One and Two but focus their assessment on the results of Alternative Two. Alternative Two is a year-by-year analysis, rather than a snapshot in time, and this gives utilities the flexibility to develop and present a realistic financial plan, cash flow forecast, and rate projection that is consistent with their fiscal policies, capital funding, and financing practices. This allows utilities to demonstrate how high and how quickly utility rates and customer bills would need to rise under various Clean Water Act implementation schedules and shows regulators how the utilities’ debt burden and other financial metrics (e.g., debt service coverage and cash reserve levels) will be impacted under various implementation scenarios, like the example provided in Figure 1. The customer bill impacts can then be compared to customer incomes to assess affordability burdens over time.

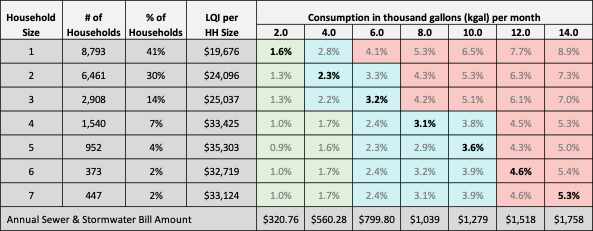

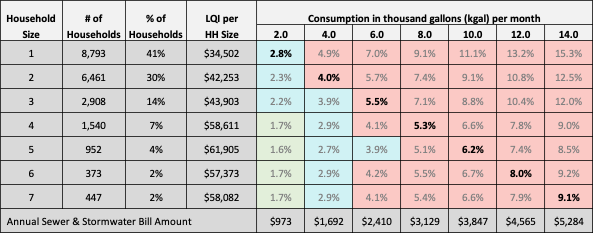

In addition, under Alternative Two, utilities can demonstrate how much of the income of lower-income households of various household sizes will need to be dedicated to paying for sewer and stormwater bills in each year of the forecast period, like the examples in Figures 2 and 3. This can help show the affordability burden across a wide range of household sizes.

The analyses incorporated into Alternative Two provide a much more complete picture of a utility’s projected financial position and customer impacts of implementing the required regulatory-driven capital investments than Alternative One. These financial forecasting details can be highlighted and used to negotiate Clean Water Act implementation timelines, making Alternative 2 a much better choice for completing the FCA for most utilities.

Since the new EPA Guidance was released in February 2023, Raftelis has completed several analyses using the FCA Guidance, and these analyses have been submitted to state and federal EPA enforcement offices for the purposes of Water Quality Standard decisions and for negotiating implementation timelines for enforcement agreements. In recent discussions, the EPA has confirmed that it will not view or use the results of the FCA as a rigid metric that will point to a specific schedule length or threshold over which the costs are deemed unaffordable. Rather, the EPA stated that it would consider each community’s financial capability on a case-by-case basis and may agree to implementation schedules that differ from the schedules that are suggested in the new EPA Guidance. Only time will tell how the regulatory agencies will evaluate and consider Alternative Two in their decision process and timeline development, but we look forward to the opportunity to include sound financial planning and utility rate considerations in the negotiations of realistic Clean Water Act implementation timelines.

Link copied