6

minute read

With the decreasing availability of federal and state grants, it has become increasingly crucial for local governments to evaluate all financing options.

One such option is the EPA's Water Infrastructure Finance and Innovation Act (WIFIA) program, but the decision to pursue a WIFIA loan is complicated. The right answer depends on a utility's specific circumstances, its credit profile, and the relationship between taxable and tax-exempt interest rates. It is very important to evaluate all the requirements for WIFIA financing relative to your other financing options.

WIFIA is designed to accelerate investment in water and wastewater infrastructure by providing federal credit assistance for projects that address regulatory compliance, water quality, drought or flooding, and aging infrastructure. On paper, it is attractive, but six factors make the comparison against traditional tax-exempt bonds complex.

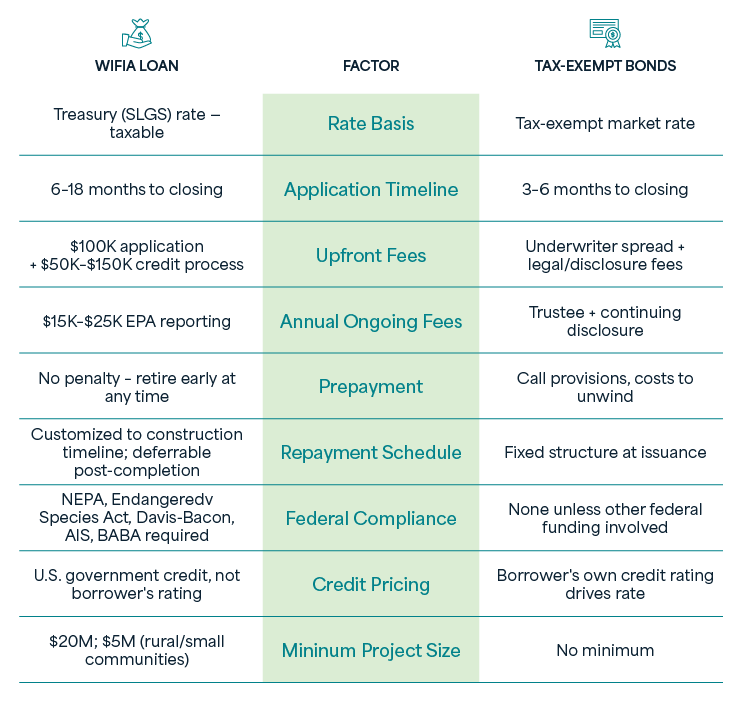

Where WIFIA truly separates itself is in its structural flexibility. The loan carries no prepayment penalty, so a utility can retire the debt early without paying a premium when cash flow or reserves allow. It permits a single, customized disbursement and repayment schedule tailored to a project's construction timeline, with repayment deferrable until after substantial completion. It also allows re-amortization and cost-effective refinancing if conditions change. For a utility that anticipates shifts in its financial position, rate adjustments, growth in its customer base, or future opportunities to accelerate debt retirement, this flexibility carries real value. It serves as risk mitigation, giving management room to respond to conditions that are difficult to predict at closing. Traditional bonds, by contrast, lock in a fixed structure with call provisions that limit early repayment and often impose costs to unwind.

WIFIA's other main appeal is its cost of capital. Because the loan rate is pegged to comparable-maturity Treasury securities at closing, it can closely compete with, and sometimes beat, the all-in yield a utility would secure in the public market.

During a recent analysis for a client who is already required to comply with federal rules (outlined below) and has a bond rating in the “A” range, the two pathways yield broadly comparable overall costs, which is why the decision turns on factors beyond the headline rate.

Public bonds can deliver very competitive rates in a favorable market but expose the issuer to timing risk: rates can move before pricing, and a utility has limited control over the market on any given day. WIFIA's more predictable rate structure insulates borrowers during the lengthy application process, which is valuable for large, long-horizon projects.

[[CTA:subscribe]]

WIFIA’s advantages come with meaningful obligations. Its application process is more burdensome than a standard bond issue, requiring NEPA review and compliance with additional federal rules. For utilities already using federal grants, these requirements may add little incremental burden because the utility may already be complying with these rules due to the requirements of federal grants. For utilities without federal funding, they create new work and cost. The larger differentiator is staff time. WIFIA can take 6 to 18 months from invitation to closing and requires sustained coordination, data collection, consultant management, and reporting. By contrast, public bond issuance typically takes 3 to 6 months and focuses mainly on disclosure and legal review. Utilities must assess whether they can manage WIFIA’s ongoing compliance obligations.

WIFIA is not categorically better than tax-exempt bonds. Though its competitive rate, absence of prepayment penalties, customizable structure, and rate predictability make it compelling for many projects, particularly where the utility already faces federal compliance or values long-term flexibility. Additionally, WIFIA is very competitive for borrowers with a weaker credit profile, where the value of leveraging the U.S. Treasury’s credit strength is used to set the rate on the financing.

The right answer depends on project size, existing funding sources, internal capacity, and a utility's appetite for flexibility versus simplicity. A disciplined, side-by-side analysis of the cost of capital, and the full set of program requirements is the only reliable way to determine the best fit for your organization, and that is the kind of evaluation Raftelis is built to support.

This article was authored in part by our intern Max Cowan, as part of our Raftelis Internship Program. Max is in his junior year at Fordham University in New York, majoring in Finance.

For more information on if WIFIA is right for your utility, contact Chad Cowan at ccowan@raftelis.com or Delaney Ridgley at dridgley@raftelis.com.

Link copied