Authors:

Henrietta Locklear, Vice President (Email)

John Mastracchio, Vice President (Email)

Across the country, utilities have suspended collections activities on utility accounts as the COVID-19 pandemic flared, schools and businesses shut down, and unemployment soared. What will this aspect of the pandemic mean for utilities? How can utilities re-enter the collections arena as states reopen?

Affordability has been a hot topic in the water utility industry for years, but the conversation around affordability itself is changing rapidly as utilities wrestle with how to respond to the new economic climate and their customers’ needs. It is vital to immediately begin understanding and planning for a potential tsunami of delinquent accounts and develop a play book for how to respond…NOW!

Gathering and analyzing data while simultaneously understanding legal constraints and developing and analyzing policy options is a key feature of deciding how to proceed in this new and sensitive landscape. Because today’s delinquency challenge is very different than a typical customer non-payment issue, deciding upon a course of action will also require communication and outreach with stakeholders and customers. Many utilities are seeing delinquencies at much higher percentages than the 0.5% benchmark, and nonpayment is occurring for customers that have never had to seek assistance before. In addition, commercial customers are not paying their utility bills. Compounding this is the reality that many utility customer assistance programs are not targeted to these types of customers.

While many utilities have existing processes and procedures in place that have historically addressed the delicate balance between delinquency and affordability, the impact of the pandemic means existing approaches must be reviewed. Analyzing data and developing new policies to address future needs for account delinquency management and customer assistance programming is a critical need for some utilities.

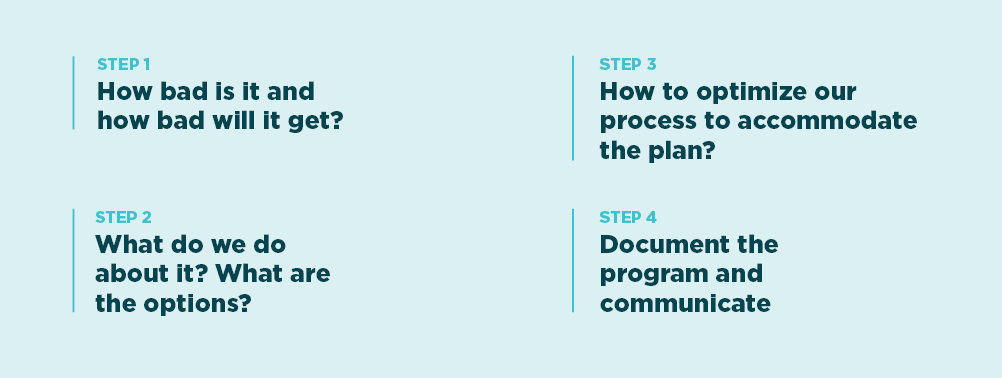

Understanding the situation in detail and tracking trends over time will inform policy options and decisions. Gaining a clear picture of the situation requires a rapid assessment of the data associated with:

Since conditions are changing rapidly, data will need to be compiled and updated almost continuously, so it will be important to set up repeatable data extraction and analysis processes and models to support continued analysis and changes in policy direction if they are needed.

Baseline data related to the extent and severity of delinquency data enables utilities to identify and assess policy options for managing delinquencies and supporting customers with payment issues.

It is important to consider existing delinquency policies and customer assistance programs, if applicable, and assess their efficacy. Have current policies been effective for the utility and helpful for customers? Do they still function well in the current environment?

Having examined existing policies, the next step is to identify any new or changed options regarding payment plans, shutoff moratoriums, returning accounts to service, late payment penalties, payment methods, bill forgiveness and so on. Options must include how to structure payment plans and over what time period, and which customers are eligible for payment plans.

The utility must also assess the timing for resuming collections activities such as shut-off and late payment penalties. Timing may be sensitive and again will involve balancing customer circumstances and other factors. An important factor in weighing policy options is to identify and consider practices of other regional and peer utilities and state and regional guidance and requirements.

The options should be developed and considered, and actions should be selected. In some cases, short-term policies and longer-term policies may need to be adopted. The selected polices should be associated with a plan of action, goals of the policies, plans for measurement and measures of success.

With policies established and plans of action in place, the next step is to ensure that the organization is adequately prepared to implement the plan. This requires ensuring the organization has the infrastructure and organizational capacity to implement the policies. Keys to success for this step include:

Continuously reviewing and optimizing workflow processes is critical to successfully support policy implementation.

Finally, the agreed upon program and policies must be documented, communicated, and rolled out. The delinquency and customer assistance policies can be packaged into an overall, holistic program. The utility’s approach and policies and customers’ opportunities for assistance will need to be communicated clearly. A best practice is to develop an outreach and communication plan targeted to impacted customers to maximize customer participation in the program.

The COVID-19 pandemic’s impact to utilities has accelerated the need to move quickly toward establishing best practice approaches to balance both service affordability and delinquency account management.

For more on our assistance to clients on delinquency account management and customer assistance programming, visit www.raftelis.com/insight/delinquent-account-management-plan-and-customer-assistance-programming.

Get more resources to help you address COVID-19 challenges at www.raftelis.com/covid-19-resources.